Different borrowers may have different loan requirements. Opting for a loan is a big commitment and it requires appropriate analysis and research before procuring a loan especially for first-time applicants.

The tenure of a loan determines many of its features, like the interest rates, the loan eligibility, the borrower’s EMI amount, and most importantly, the loan repayment terms.

There are multiple categories to define loans depending on the purpose of the loan seekers but ultimately there are two main types of loans. A loan can be taken for a long term or short term commonly termed as repayment tenure. Short-term loans are those which are taken for a short tenure of fewer than 12 months.

These types of loans are usually one-time loans procured to finance a particular business or personal need. Such loans are generally taken when you cannot obtain credit from a bank for a longer tenure loan or the required amount is not big.

A short-term loan can be helpful and have multiple advantages over the use of credit cards and other forms of instant credit or loans from financial institutions in certain situations or needs. Short-term loans may generally be taken for a variety of reasons like unexpected expenses, repayment of credit card dues, two-wheeler purchases, and many other reasons.

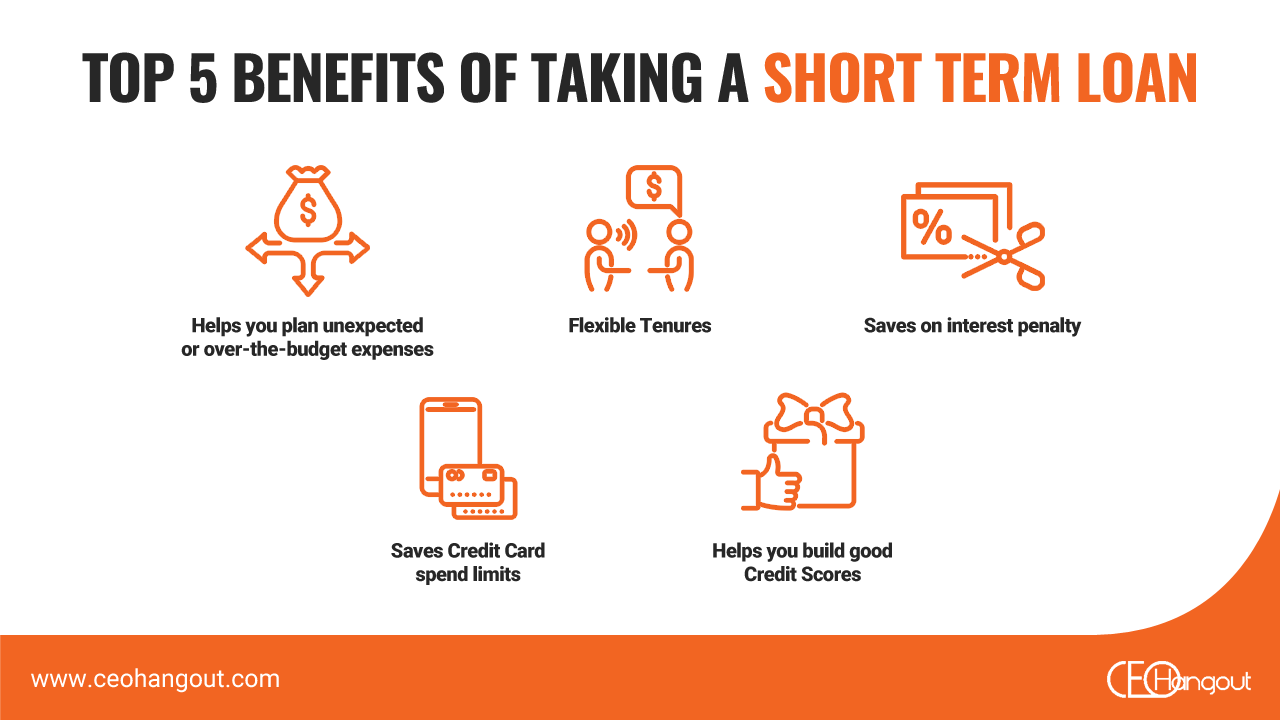

Short-term loans have a lot of benefits but overall, it comes down to the requirements of the borrower and available credit solutions in the market. Short-term loans can help a borrower in more than one way, in this post we’ve compiled 5 ways a short-term loan can be beneficial for a credit or loan seeker.

Let us now start with the list of these benefits:

1. Help You Plan Unexpected or Over-the-Budget Expenses

A short-term loan is a valuable borrowing option for individuals and entrepreneurs alike.

Small businesses that are ineligible for a bank credit line or individuals who face an unforeseen financial problem may need such loans that where a smaller sum of amounts need to be borrowed. They can turn to short-term loans to help them out and see them through until they can get back up.

One of the most famous short-term loans is a car title loan. As the name suggests, these types of loans allow you to get access to quick cash using your car or vehicle title as collateral. In case of emergency, these kinds of short-term loans can become a lifesaver since they are the most convenient solution in an urgent money need.

These loans usually help to resolve sudden cash flow crunches or capital needs for businesses. They can also serve as an effective means of emergency or contingency funds for individual borrowers as short-term loans are usually faster in terms of approval and processing compared to personal loans with bigger amounts and longer tenures.

2. Flexible Tenures

Short-term loans as mentioned above are loans availed for shorter tenures, usually ranging from 3 to 12 months. The loan can be conveniently paid off in tenures that the borrowers may find suitable as per their repayment capabilities, ranging from three months to a year.

Some lenders may extend credit to 18 months as well while some short-term loan products can have even lesser tenures such as microloans or advance salary loans. Some lenders may not specify the payment schedule for these loans or may not have a fixed payment due date.

This feature gives the borrowers a chance to repay their loans at their convenience. It becomes easier for a borrower to plan a budget for the repayment of a short-term loan and effectively cut down some additional costs.

3. Save on Interest Penalty

Interest payments and EMI’s are the deciding factors for paying off a loan. Short-term loans have lower total interest payments as they have short tenures of periods below a year.

Also, in this case, the interest paid comes out to be significantly less as compared to that for long or medium-term personal or business loans. This arrangement allows borrowers to save money in two ways: both the rate at which the interest is applied and the time it has to occur.

The longer is the loan tenure, the more interest is added to your payoff balance that you need to pay back to the lender. A shorter loan term allows you to pay back your loan quicker and at lesser total interest compared to a loan of a similar amount but longer tenures.

Thus, even though the interest rate for short-term loans is higher than a long-term loan, you can save money on interests in the long run due to less time for which the interest is accrued.

4. Save Credit Card Spend Limits

Personal loans and credit cards both offer a way to borrow funds giving credit seekers access to easy and instant credit. They also have the same credit provisions. However, Credit cards are a lot different from personal or short-term loans, they are a type of revolving credit.

It means that the borrower can access the funds up to a specified amount as long as his account remains in good standing. The borrower does not get the full credit amount but can take funds from the account up to or close to the maximum credit limit.

Credit card interest rates are usually higher than those for personal loans. The interest rate depends on your card’s APR (Annual Percentage Rate). If your APR is high, your interest charges will also add up. Your monthly payment for credit cards will be variable each month depending on the consumed limit or spend, whereas, for short-term loans, it will be the same over the entire loan tenure. Therefore, using short-term loans can be beneficial instead of using a credit card for bigger purchases.

5. Helps You Build Good Credit Scores

Short-term loans are favorable for both borrowers and lending institutions as the risk factor involved is less in comparison to long-term loans and the processing time is faster. Due to a short tenure, the borrower can maintain his loan repayment ability with ease, which will not change much over a short period.

Short-term loans also serve as a lifesaver for individuals or small business enterprises who do not have impressive credit scores for loans with bigger amounts and longer tenures.

Overall, if you acquire a short-term loan and promptly pay it off in time, it will be positively reported back to the credit bureau by the lending institutions and will help improve your credit score quickly and effectively leveraging your ability to take bigger loans.

Now, you know the important benefits of taking a short-term loan. We will be taking a look at some of the most common types of short-term personal loans that people often look for.

Micro Loans: A Ray of Light

Microcredit or Microloans are a type of small loan extended to borrowers who lack steady employment and have low incomes. They also do not have the facility to provide collateral or verifiable credit history.

In such scenarios, they may face difficulties in securing credits from banks or other credit agencies. Microloans are offered to provide timely capital to small entrepreneurs, below the poverty line, in times of need to support their business requirements.

Microloans are based on relationship-based banking for SMEs and individual entrepreneurs. They are built upon group-based lending models, where several entrepreneurs come together to apply for loans as a group.

Reliable P2P lending platforms often help people with an average credit scores or even no credit history get access to instant credit. And unlike banks, credit seekers can get funds from individual lenders.

Advance Salary Loans

Advance Salary loans are a type of short-term loan against your salary, provided to meet some urgent or unexpected personal needs. These loans are generally meant for salaried individuals who need extra capital to meet an unexpected financial requirement.

The loan amount can be as high as 2.5 times the individual’s net salary and can range from Rs. 25,000 to Rs. 1 lakh or even more depending on the salary and credit score of the applicant. The actual amount of the extended loan depends upon the credit checks, and the borrower’s income, and current debts.

The borrower can repay the loan amount in full with interest in the next month or with monthly installments as per the loan agreement. Advance salary loans are swift to get and easy to procure online. With a record of prompt repayments, credit seekers can get bigger limits and faster approval on top-up loans.

So, these were some of the major benefits of getting a short-term loan. We have also shared the two common types of loans that have only come into existence in recent years, and credit seekers are greatly using them for their advantage.

As fintech companies continue to evolve, a lot of great options have emerged for credit seekers and many more new forms of credit options will emerge in near future contributing toward the financial inclusion of every eligible citizen.

If you have any queries or about short-term loans or any other questions related to credit and loans, you can share your queries in the comments and we will be happy to discuss and help you with your queries.

Author Bio

Himanshu Sharma is a Growth Advisor at Lendbox that is a leading P2P company in India. Lendbox also offers diverse short-term loans to meet customers’ varied loan requirements.